Home > Opinion > Why Mbah’s Tax Reversal Fails the Test...

Why Mbah’s Tax Reversal Fails the Test of Credibility and Timing

By Admin | 09 Apr, 2026 06:18:12am | 369

By Dr. Buchi Nnaji

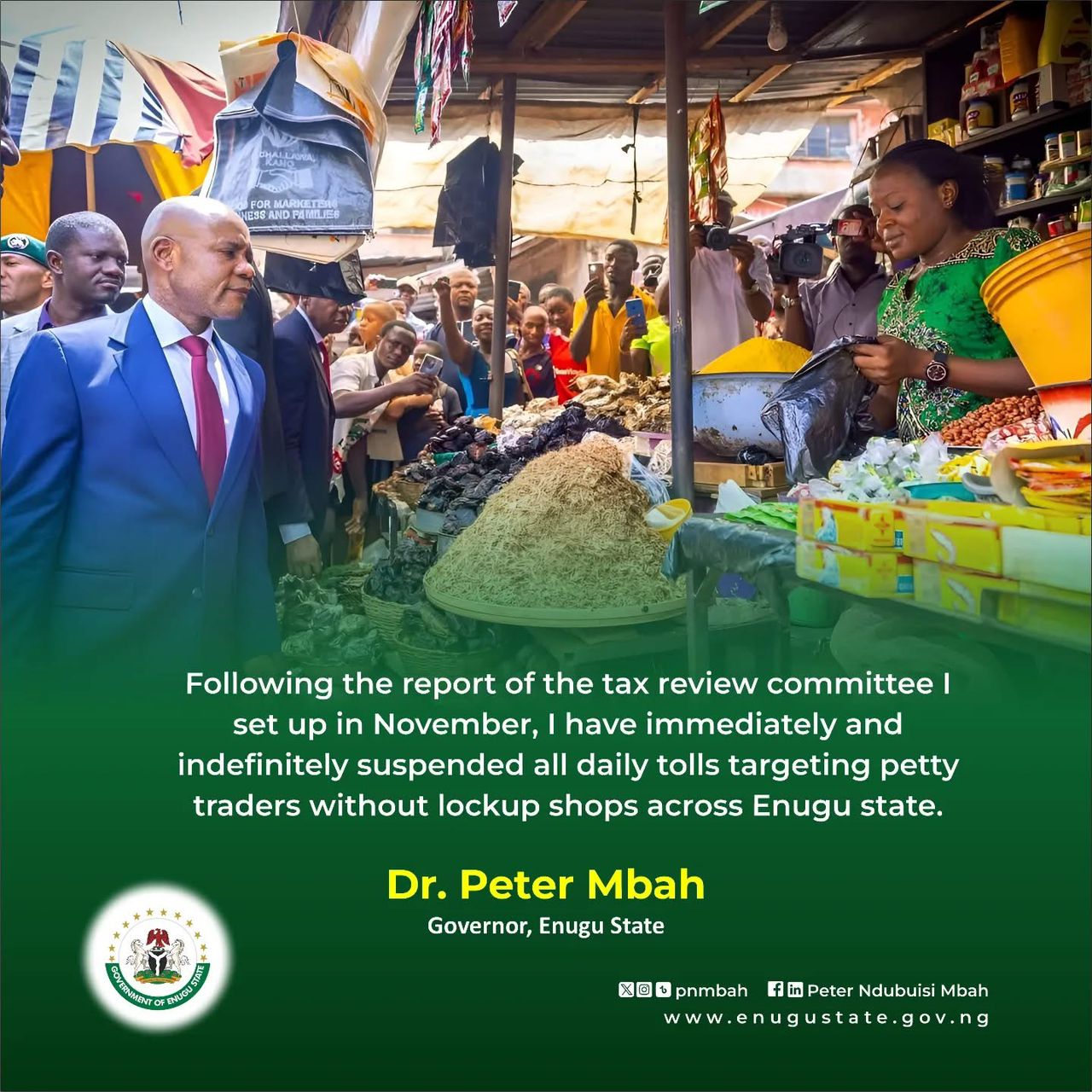

The recent decision by Peter Mbah to suspend daily tax collections on petty traders without lock-up shops marks a notable policy shift that has sparked debate over its intent, scope and sustainability.

For more than two years, residents and small-scale traders in Enugu State have raised persistent complaints about multiple taxation, illegal levies and aggressive revenue collection practices. These concerns gained institutional recognition with the passage of the Enugu State Harmonised Taxes and Levies Law, 2026, which sought to eliminate unauthorised collections and dismantle roadblocks used for illegal revenue enforcement. The legislation itself underscored the depth of public dissatisfaction and the extent to which informal taxation had become entrenched.

Despite these concerns, the Mbah administration had consistently dismissed claims of over-taxation, describing them as misconceptions and maintaining that its policies were focused on expanding the tax base and improving internally generated revenue. However, the recent suspension of daily levies on petty traders appears to contradict that position, effectively acknowledging that elements of the existing system were either excessive or improperly enforced.

The inconsistency between earlier denials and the current policy reversal raises questions about governance coherence. A government that previously rejected claims of over-taxation has now implemented a measure that directly responds to those same grievances, thereby weakening the credibility of its earlier stance.

More significantly, the relief measure is limited in scope. While traders without lock-up shops have been exempted from daily levies, those operating from lock-up shops remain subject to annual charges reportedly ranging from ₦30,000 to ₦36,000. This selective application highlights a fragmented approach to reform, as it addresses only a segment of affected traders while leaving the broader tax structure largely intact.

The implication is that the policy functions more as a symbolic concession than a comprehensive restructuring of the state’s revenue system. By targeting the most vulnerable group, the government alleviates immediate public pressure without undertaking deeper institutional reforms that would address the root causes of multiple taxation and enforcement abuses.

Under the current administration, the state’s internally generated revenue has recorded significant growth, rising from ₦26.8 billion in 2022 to over ₦400 billion in 2025. While this increase has been presented as evidence of fiscal efficiency, it also raises concerns about the burden placed on citizens, particularly within the informal sector, which constitutes a large portion of the state’s economy. Expanding the tax net in such a context, without corresponding improvements in income levels, risks imposing regressive pressure on already vulnerable populations.

The timing of the policy shift further complicates its interpretation. With the 2027 election cycle approaching, the suspension of daily levies on petty traders may be viewed as a calculated move to rebuild public trust and appeal to grassroots voters. Such policy adjustments are not uncommon in pre-election periods, where governments often soften fiscal measures to consolidate political support.

Equally important is the question of sustainability. The suspension appears to be an administrative directive rather than a deeply entrenched legal reform, making it susceptible to reversal. In the absence of structural changes to the tax framework, there remains the possibility that the policy could be altered or withdrawn in the future, potentially replaced with new or even more stringent revenue measures.

This uncertainty underscores broader governance concerns, including issues of policy consistency, institutional credibility and the risk of politically motivated decision-making. While the suspension of daily levies offers immediate relief to a segment of traders, it falls short of addressing the systemic challenges associated with taxation and revenue collection in the state.

In its current form, the policy represents a limited intervention rather than a comprehensive solution. A more enduring approach would require transparent tax structures, the elimination of informal and illegal levies across all sectors, and legal safeguards to ensure that reforms are not subject to abrupt reversal.

Until such measures are implemented, the recent decision may continue to attract scrutiny as a short-term adjustment shaped as much by political considerations as by economic necessity.

Leave a Reply

Your email address will not be published. Required fields are marked *

Category

Opinion

Opinion Technology

Technology Education

Education  Entertainment

Entertainment News

News Sports

Sports  Religion

Religion  Crime & Security

Crime & Security Culture & Tourism

Culture & Tourism Health

Health.jpeg) Interviews

Interviews Politics

Politics Business & Economy

Business & Economy